Italian GDP is expected to grow after three years of contraction. Domestic demand is forecast to stabilise as investments and household consumption are expected to accelerate.

The insolvency environment

Italian business insolvencies are expected to increase 10% in 2015.

Corporate insolvencies have increased sharply since 2008, up 10% year-on-year in 2014. In 2015 we expect Italian business insolvencies to again increase by 10%, with construction, civil engineering, metals and wholesale/retail (mainly furniture, household appliances, clothing and footwear) still the worst affected sectors. Liquidity problems of Italian businesses are exacerbated by continuing poor payment behaviour, especially by the public sector. Moreover Italian companies, compared to their Western European counterparts, show a higher average gearing - especially short-term gearing. Many businesses suffer from the currently restrictive loan policies of many banks, and this is expected to continue into 2015. The structurally high dependence of Italian businesses on bank financing is proving to be a major structural weakness.

Construction and retail still show a negative trend in probability of default.

Economic situation: is there a rebound on the horizon?

The economic downturn continued in 2014

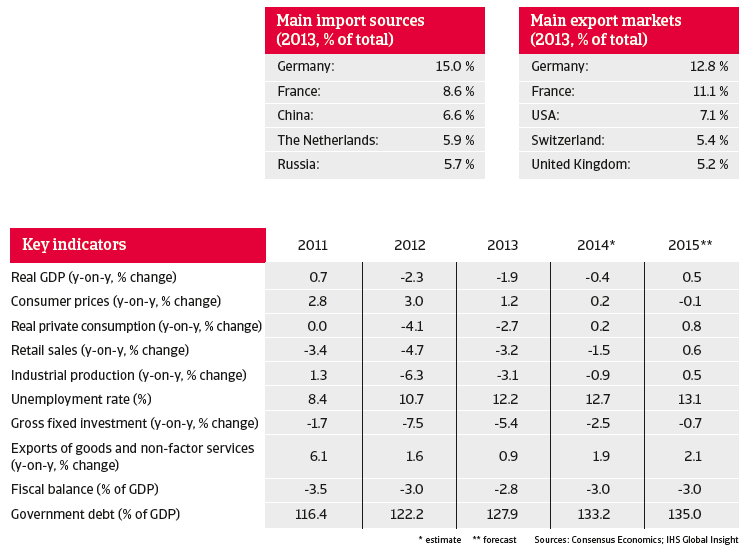

After a 1.9% contraction in 2013 the Italian economy shrank again in 2014, by 0.4%. However, private consumption rose 0.2% after the sharp drops of more than 4% in 2012 and 2.7% in 2013, when disposable income shrank and consumer confidence reached its low point. Investments continued to decrease (down 2.5% in 2014) in an atmosphere of difficult financing conditions and poor business confidence. Foreign demand provided only limited support to growth, however, with lower imports, net exports were a positive contributor to GDP growth in 2013 and 2014 (see chart below).

Slight growth expected in 2015

In 2015 GDP is expected to grow again after three years of contraction, by 0.5%. Domestic demand is expected to stabilise as investments are expected to pick up and growth in household consumption is forecast to accelerate to 0.8%. Households´ available incomes have started to increase again at the end of 2014. This is partially due to a EUR 80 monthly tax break for low-paid employees introduced by the government in May 2014. However, unemployment is forecast to remain stubbornly high (13.1%) in 2015. Exports are expected to increase 2.1% in 2015. Consumer prices are expected to decrease slightly, by 0.1%, in line with an overall decline in the Eurozone.

Less pressure on international competiveness?

Mainly as a result of a significant decrease in imports, Italy ́s current account deficit became a current account surplus in 2013. In 2015 the surplus is expected to grow to 1.7% following the 1.6% surplus in 2014). An increase in exports is supporting this improvement, but it is mainly thanks to still subdued imports.

Italy has lost nearly 20% of its share of its export markets - particularly European markets - over the last couple of years, although it has retained its leading position in fashion, clothing and textiles.

This loss of market share is borne out by Italy’s Real Effective Exchange Rate (REER) development. The REER measures a country’s international competitiveness as costs and prices change. Italy’s competitive position against some other Southern European countries further worsened in 2013 and 2014, as those markets implemented more reforms to reduce their unit labour costs.

That said, Italy´s productivity is set to recover somewhat. Given the still high level of unemployment, wage rate growth should be limited. As a result, unit labour cost (which is part of the REER) is expected to improve in 2015.

Italy‘s productivity is set to recover somewhat.

The banking sector remains vulnerable

When the Eurozone crisis deepened in the fi rst half of 2012, Italian banks had to rely increasingly on the European Central Bank (ECB) for funding. While the ECB’s liquidity provisioning remains considerable, it has decreased in 2014. Since 2009, non-performing loans as a percentage of regulatory capital have sharply increased, indicating stress in the banking sector. That said, there is some light at the end of the tunnel as the ratio of new bad loans is now lower than in the past. However, the volume of loans to the private sector continues to contract, due to still tight credit standards and high borrowing costs. In particular, loan provisions to smaller businesses remain constrained.

Government debt remains very high

Down to below 3% of GDP since 2012, the yearly Italian budget deficit has reached healthier territory. In 2015 a deficit of slightly below 3% of GDP is expected. However, the subdued economic performance impacts a sustainable increase in the already high government debt/GDP ratio. Despite successful fiscal consolidation, this ratio increased to 133.2% in 2014 from 127.9% in 2012. This was due mainly to the economic contraction, and is therefore expected to rise again to 135 % of GDP in 2015. In order to decrease the ratio substantially a nominal annual growth rate of 3% would be required. The challenge is achieving the required high level of real growth, while also pursuing fiscal consolidation and in a low inflation environment.

Bond yields have decreased significantly

Following fears of a Greek exit from the Eurozone in May 2012, Italian government bond spreads leapt quickly to levels considered unsustainable, as financial markets feared that Italy would be part of a Eurozone breakup. However, the June 2012 summit of Eurozone leaders confirmed a number of measures to reinforce the Eurozone. Crucially, the European Central Bank gave its backing by announcing that it would do ‘everything it takes’ to prevent a breakup, including a government bond purchase programme. This has calmed financial markets, and bond yield spreads over the German bunds have decreased significantly since then (see chart below).

More reforms needed

In December 2014 the Renzi administration successfully passed a bill that gives the government a mandate to push ahead with labour market changes without then going back to Parliament for fi nal approval. While the plans have remained vague so far, they have nevertheless met the opposition of trade unions and parts of Renzi´s own Democratic Party. The current labour market regulations still provide a solid protection for those workers on permanent contracts. Because newly hired staff on a permanent contract have the same protection as those who have worked for a company for 30 years, firms are still shying away from such contracts. With many young employees on temporary contracts, productivity is decreasing, not least because companies are less willing to invest in training temporary staff.

At the same time legal initiatives to improve judicial efficiency, expand deregulation and contain red tape have been limited so far.

Documents associés

2.81MB PDF